How to declare crypto in Switzerland

Confused by Swiss crypto taxes? Learn how to report Bitcoin, ETH, and DeFi assets for 2026. Understand wealth tax vs. capital gains and avoid common filing errors in your canton.

![]() 6 minutes|Yann Gerardi|Published 2023-03-22|

6 minutes|Yann Gerardi|Published 2023-03-22|

Disclaimer: The content of this page is provided for informational purposes only and does not constitute legal or tax advice. For tax advice and other related services, please contact a qualified professional. Furthermore, while we make every effort to keep the information provided up to date, we cannot guarantee the same because government tax practices may change without our knowledge. We are not liable for any decisions or actions you take based on the information presented on this page.

Table of contents

- Introduction

- Crypto mining

- Staking

- Airdrops

- NFTs

- MPS tokens

- Capital gains

- How to declare

- Self-denunciation

- General tips

- Need help?

- FAQ

Introduction

Source: Federal Tax Administration

The Swiss fiscal authority considers that there are three different types of crypto-assets:

- Payment tokens

- Investment tokens

- Utility tokens

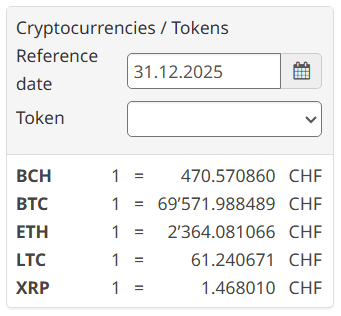

Whatever the type of crypto-asset that you own and wherever it is stored (without exception), you must declare its market value on December 31st in your wealth.

The fiscal administration provides the market value of the main cryptocurrencies here, for the others you will need to find it yourself (you can easily find them on Coingecko here).

If you don't find it, you must declare its purchase value converted in Swiss Franc.

In principle, it is usually acceptable to declare the total value of your crypto holdings without reporting the detail.

Crypto mining

Cryptocurrencies acquired through mining activities are considered as remuneration in Switzerland, meaning that you will need to declare them as revenue from an independent lucrative activity.

Staking

Cryptocurrencies that you stake must be reported in your wealth, as explained above. As for the revenue generated by the staking activity:

- If you stake through a pool, the earnings must be declared in your wealth revenue at their market value in CHF at the moment you receive them.

- If you are a solo staker, the earnings must be declared as revenue coming from an independent lucrative activity.

Airdrops

If you have received an airdrop, you must declare it at its market value in CHF at the moment you receive it, as wealth revenue. For the following years, simply declare the crypto you have received in your wealth.

NFTs

For the time being, the official documentation don't give specific guidance for NFTs. In the meantime, you must declare NFTs you own in your wealth at their market value if it exists, if not at their purchase value in CHF.

Declaring MPS tokens

The MPS token is the actual share of Mt Pelerin Group SA. Therefore, you should declare and report it in your tax return the same way as you would for the ownership of the shares of any other non-public limited company.

Each year, we communicate the fiscal value of the MPS by email to registered shareholders, which is determined by our Swiss cantonal administration.

That value must be used to declare your tokens in the shares or securities section of your tax report.

Capital gains

Capital profits and losses realized as an individual are exempt from tax and are not deductible in Switzerland.

However, if you are more than a casual investor/miner you might be qualified as a professional (activité lucrative indépendante). In such a case, you won't be subject to wealth tax anymore but to income tax.

Many factors come into play for that qualification so there is no single answer to how it works, however the tax administration will typically look at your number of trades per day, whether you borrow and leverage funds to trade, and whether the gains from that activity are the main source of income for your living standard or not.

More information can be found about that qualification process in the Federal circular no.36.

How to declare cryptocurrencies

In Switzerland, tax declarations are made at the cantonal level and each canton provides different reporting tools, but they all have a similar structure.

You will find a section for independent activities that you will use to declare your mining activities, and a section for your wealth. Its name and aspect might vary, but in principle you should find:

- An "account" section, where you can declare your accounts on centralized exchanges (Binance, Kraken, etc) just like a regular bank account.

- A "money" section, where you can declare the cryptocurrencies that you own in self-custody, just like you would declare cash or gold.

- A "security" section, where you can declare your investment tokens (like the MPS) alongside shares and bonds. Any token that you have invested in during a token sale and that provides a social (like voting) or economic (refund, yield, dividend, revenue sharing, etc) right is considered an investment token.

- A "wealth revenue" section, where you can declare your revenues from staking, yield and airdrops.

Self-denunciation: what if you have never declared your crypto?

If you need to convert an important sum of crypto into fiat (to buy a house for instance), you will need to justify the origin of those funds and show as well that you have properly declared them in your taxes until now.

If you've never declared them before, you can do a «spontaneous denunciation» procedure (this is a once in a lifetime trump card) that will spare you fines, although you will need to pay taxes and interests retroactively of course.

General tips

- You can export your crypto-fiat transactions made with Mt Pelerin in PDF or CSV format on app.mtpelerin.com by going in the transactions tab, then click on "Export".

- You can export your crypto-fiat transactions made with Mt Pelerin in PDF or CSV format in our mobile app Bridge Wallet by going in the transactions screen, select the "bank transfer" tab and click on "Transactions statement".

- You can export your crypto-to-crypto transactions from most block explorers.

- Take a screenshot of your crypto holdings each December 31st. For the Ethereum ecosystem, you can easily do that by pasting your public address on Debank (it's free and without registration).

Need help with your Swiss tax declaration?

Fill the form below to request a free consultation with the specialized tax advisory firm Imperial Wealth Planning GmbH:

FAQ

How do I declare my cryptocurrencies in my 2026 Swiss tax return?

In Switzerland, you must declare the market value of all crypto-assets held as of December 31st as part of your wealth. Use the official exchange rates provided by the SFTA (Federal Tax Administration). If a specific cryptocurrency is not listed, use the CHF value from a reliable source like Coingecko or its original purchase price.

Do I need to declare Mt Pelerin as an account?

No, Mt Pelerin is a non-custodial exchange service: you buy, sell, and swap your cryptos directly from a wallet that you exclusively control. Mt Pelerin never holds your funds and does not operate as a deposit account. Consequently, there is no need to declare it as a bank account or as a crypto-asset account, even if you have been assigned a personal IBAN. Of course, this does not exempt you from your general tax obligations. If in doubt, we recommend consulting a local tax advisor.

At what value should MPS tokens be declared?

MPS tokens must be declared at their official tax value, which is determined by the tax authority of the canton where Mt Pelerin is based. This value is generally communicated to registered shareholders every year. If no value is available at the time of your declaration, the tax value from the previous year may be used as an indication.

How should I declare Mt Pelerin's MPS tokens?

The MPS token represents a share in Mt Pelerin Group SA and must be declared in the "securities" or "shares" section of your tax return, just like any other company share you might own. Use the specific tax value communicated by Mt Pelerin via email, which is determined annually by the Swiss cantonal tax administration.

Does Mt Pelerin share my information with tax authorities?

As of today, Mt Pelerin does not automatically transmit tax information to any Swiss or foreign authorities. However, Switzerland plans to introduce the OECD's Crypto-Asset Reporting Framework (CARF) starting January 1, 2027. Under this regime, data regarding crypto transactions could be transmitted starting in 2028. Only transactions carried out as of January 1, 2027, would be affected (no retroactivity).

Do I need to declare every crypto transaction to Swiss taxes?

No. In Switzerland, taxpayers must declare the total value of their crypto-assets as of December 31st of each year. Individual transactions do not need to be reported separately within the standard framework.

Do I need to declare my crypto capital gains to Swiss taxes?

In principle, no. Capital gains realized by private individuals are not taxable in Switzerland. However, if your activity is classified as professional (e.g., frequent trading, use of leverage, structured organization), the gains become taxable and must be declared.